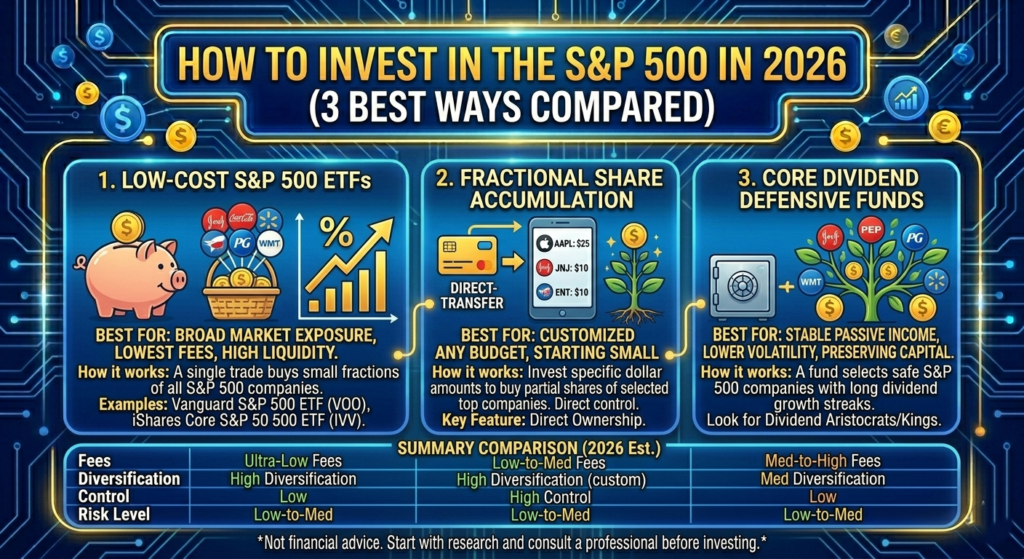

f you want to know how to invest in S&P 500 and nothing else, there are three main routes in 2026, all of which get you the same core benchmark: the S&P 500 Index. You can:

- Hold an S&P 500 ETF (VOO, SPY, or IVV).

- Use an S&P 500 mutual fund (FXAIX, SWPPX).

- Run the same exposure inside a Roth IRA, 401(k), or taxable brokerage.

You’ll walk away knowing:

- A head‑to‑head comparison of VOO, SPY, and IVV by expense ratio and liquidity.

- How Fidelity FXAIX (0.015%) and Schwab SWPPX (0.02%) fit in.

- Which account type gives you the best tax treatment for S&P 500 exposure.

- What $500 per month for 30 years at 8% can grow to (roughly $680,000).

- How to think about concentration in the biggest few stocks, no foreign exposure, and bear‑market pain.

How to invest in S&P 500: the three main routes

There is no “right” single way; there are three practical flavors of getting S&P 500 exposure:

- Exchange‑Traded Funds (ETFs):

- Buy VOO, SPY, or IVV on any major broker (Fidelity, Schwab, Vanguard, Robinhood, etc.).

- You own shares of the ETF, not the underlying stocks directly.

- Mutual funds:

- Use FXAIX (Fidelity® 500 Index Fund) or SWPPX (Schwab S&P 500 Index Fund).

- These are traditional mutual funds, not ETFs, but they track the same S&P 500 index.

- Employer plans or IRAs:

- Some 401(k)s put you into an in‑house S&P 500 index fund (or a similar large‑cap index).

- You can still follow the same logic: low‑cost, broad‑cap, S&P‑like exposure.

You can mix and match; for example, hold VOO in a taxable account and FXAIX in a Fidelity IRA.

ETF routes: VOO, SPY, and IVV

These three ETFs all track the S&P 500 Index, but they differ on fee, size, and liquidity.

1. Vanguard S&P 500 ETF (VOO)

- Ticker: VOO

- Expense ratio: 0.03%.

- AUM: Roughly $900 billion+, making it one of the largest ETFs in the world.

- Why it’s popular: Ultra‑low fee, broad S&P 500 exposure, excellent bid‑ask spreads, and Vanguard’s reputation for low‑cost indexing.

VOO is the default S&P 500 ETF for most invest1now.com in 2026.

2. SPDR S&P 500 ETF (SPY)

- Ticker: SPY

- Expense ratio: 0.0945% (Gross Expense Ratio).

- AUM: Massive, but still higher‑cost than VOO and IVV.

- Why it exists: SPY is the oldest S&P 500 ETF and has the widest options and futures market around it.

SPY is best for active traders or options users; if you’re just buy‑and‑hold, the extra 0.06% per year eaten by fees can add up.

3. iShares Core S&P 500 ETF (IVV)

- Ticker: IVV

- Expense ratio: 0.03%.

- Structure: iShares fund by BlackRock, also tracking the S&P 500.

- Why it’s solid: Same benchmark as VOO, same fee, decent liquidity, but smaller AUM than VOO.

If your broker or plan favors iShares over Vanguard, IVV is a near‑carbon‑copy alternative to VOO.

Practical tip:

- For almost everyone, VOO or IVV beat SPY on cost if you are not actively trading options.

Mutual fund routes: FXAIX and SWPPX

If you prefer mutual funds over ETFs (or your employer only offers one), these are the main S&P 500‑tracking choices.

Fidelity 500 Index Fund (FXAIX)

- Ticker: FXAIX

- Expense ratio: 0.015%.

- Benchmark: S&P 500 Index.

- Best for: Fidelity investors who want in‑house, low‑cost S&P 500 exposure with no transaction fees inside Fidelity accounts.

FXAIX is slightly cheaper than VOO on paper, but it is mutual‑fund only, so you can’t easily move it between brokers.

Schwab S&P 500 Index Fund (SWPPX)

- Ticker: SWPPX

- Expense ratio: 0.02%.

- Benchmark: S&P 500 Index.

- Best for: Schwab‑centric investors who want a no‑fee‑to‑buy S&P 500 index fund inside Schwab IRAs and taxable accounts.

SWPPX is a bit cheaper than VOO/IVV and significantly cheaper than SPY, but still not as cheap as FXAIX.

Both FXAIX and SWPPX are good choices if you’re already inside Fidelity or Schwab and don’t want to fight with ETFs.

Which account is best to hold S&P 500 in?

You can hold VOO, SPY, IVV, FXAIX, or SWPPX in three main buckets: Roth IRA, traditional IRA, 401(k), or a taxable brokerage.

Roth IRA usually wins for long‑term S&P 500 exposure

- Why:

- You contribute after‑tax dollars.

- All future growth and dividends on VOO, FXAIX, SWPPX, etc. can grow tax‑free if you hold them inside a Roth IRA. [IRS]

- Roth IRAs have no required minimum distributions during your lifetime (RMD age is 73 in 2026 for traditional IRAs and 401(k)s). [IRS]

If you have a long horizon (20–40 years), Roth is usually the best home for S&P 500 index funds.

When to use other accounts

- Traditional IRA: Good if you want an upfront tax deduction but you’ll pay tax on withdrawals later, including on S&P 500 gains.

- 401(k): If your employer offers a low‑cost S&P 500‑style fund, you can hold it there even if it’s not VOO or FXAIX.

- Taxable brokerage: Ideal if you’ve maxed out retirement options and still want S&P 500 exposure. You’ll pay capital gains when you sell and dividend taxes along the way, but the S&P 500 mostly throws off qualified dividends, which are taxed at 0%, 15%, or 20% depending on your bracket. [IRS]

Lump sum vs dollar‑cost averaging into the S&P 500

When you ask how to invest in S&P 500, you usually decide:

- Should you dump in a lump sum now?

- Or spread it out over months (dollar‑cost averaging)?

Vanguard’s research on lump‑sum vs dollar‑cost averaging gives a clear answer:

- Over long periods (1926–2015 rolling 10‑year windows), lump‑sum investing beat 12‑month dollar‑cost averaging roughly 68% of the time in the U.S. and similarly across the U.K. and Australia.

- The performance advantage is not tiny; keeping money in cash longer underperforms putting it directly into the market.

In practice:

- If you have a stable job and a diversified portfolio, lump‑sum into VOO or FXAIX is usually the better mathematical choice.

- If you’re emotionally scared of a crash or new to investing, 3–12 months of DCA can keep you from panic‑selling later.

It’s a trade‑off between expected returns and your nerves.

How much $500 per month in the S&P 500 can grow

If you commit $500 per month for 30 years into a low‑cost S&P 500 index fund (VOO, IVV, FXAIX, SWPPX), here’s roughly what that looks like at an 8% annual return (roughly 7% inflation‑adjusted, based on long‑term S&P 500 data):

- Total you put in: 30 years × 12 months × $500 = $180,000.

- Ending value at 8%: Around $680,000 (slightly over that depending on the exact assumptions).

Of that $680,000, about $500,000 is growth, not your own money.

If you lower the return to 7%, you end up closer to $570,000. If you raise it to 9%, you can push toward $800,000+.

Those numbers are not guaranteed, but they show why time in the market beats timing when you invest in the S&P 500.

worries about investing in S&P 500 (and how to think about them)

Even if you know how to invest in S&P 500, you’ll still hear people question:

1. “What about concentration in the top 7 stocks?”

The S&P 500 is not equally weighted. In 2026, a small group of mega‑caps (like NVDA, MSFT, AAPL, AMZN, META, GOOG, BRK.B) can make up a big chunk of the index.

- Reality: This is how the index works; the biggest companies have the biggest market value.

- What you can do:

- If you’re worried, add some broad‑market diversification (VTI for total U.S. market, VXUS for international).

- Or accept that you’re essentially owning the leading U.S. companies and not every small‑cap equally.

2. “It has no overseas exposure.”

The S&P 500 is U.S.‑only.

- Reality: Many S&P 500 giants (Apple, Microsoft, Nvidia, etc.) earn a big chunk of revenue overseas, but the index is still U.S. stocks.

- What you can do:

- Pair your S&P 500 holding with VXUS (global ex‑U.S. stocks) if you want explicit foreign exposure.

3. “Bear markets can wipe out years of gains.”

Yes. A sharp drop in the S&P 500 can knock 20–40% off your account in a bad 12‑month stretch.

- Reality: Bear markets are normal, not a defect.

- What you can do:

- Avoid short‑term loans against the S&P 500.

- Use bonds (BND, FXNAX) or cash to smooth out withdrawals in retirement.

- If you’re young and contributing $500 per month, a bear market is an excuse to buy more at lower prices, not to bail.

How to actually do it step‑by‑step (2026)

- Pick a broker or platform (Fidelity, Schwab, Vanguard, Robinhood, etc.).

- Open a Roth IRA or taxable brokerage if you don’t already have one.

- Decide on your S&P 500 vehicle:

- Prefer ETFs → VOO or IVV.

- In Fidelity → FXAIX mutual fund.

- In Schwab → SWPPX mutual fund.

- Choose lump sum or DCA based on your comfort and Vanguard’s data.

- Set up automatic contributions (e.g., $500 monthly to VOO or FXAIX).

If you want to see how different S&P 500 mixes and contribution schedules grow over 10–40 years,